What you need to know about he “Preliminary Term Sheet”

Key Terms

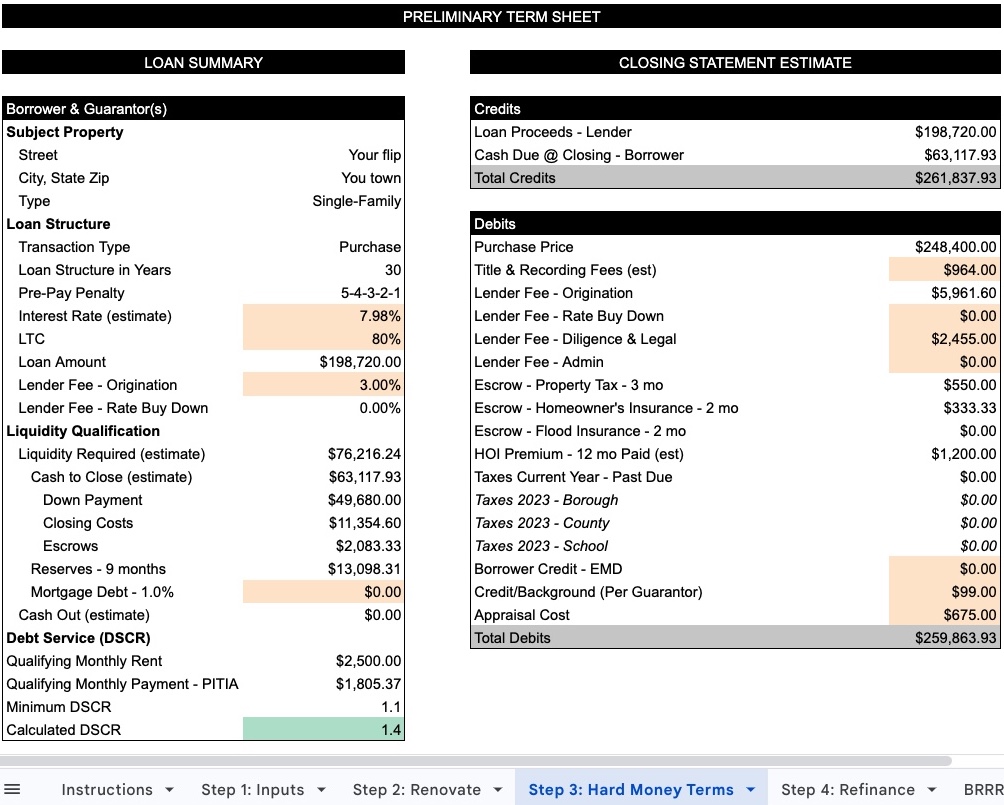

DSCR

DSCR (Debt Service Coverage Ratio) measures a property’s ability to cover its debt obligations through its income. Here’s a breakdown of DSCR in the context of hard money loans:

Calculation

DSCR is calculated by dividing the property’s Net Operating Income (NOI) by its total debt service:

DSCR = Net Operating Income / Total Debt Service

For example, if a property generates $2,500 in monthly rent and has a total monthly debt payment (principal, interest, taxes, and insurance) of $3,000, the DSCR would be: $2,500 / $3,000 = 0.83

Origination Fee

Is a charge imposed by the lender for processing and underwriting the loan. Here’s a breakdown of the origination fee for hard money loans:

Typical Range

The origination fee for hard money loans typically ranges from 1% to 4% of the loan amount. However, most lenders charge between 2% and 3% of the loan amount.

The origination fee serves several purposes:

- It covers the lender’s costs for processing the loan application, underwriting, and funding the loan.

- It compensates the lender for evaluating the deal and providing consultative services.

Calculation

The origination fee is usually calculated as a percentage of the total loan amount. For example:

- If a lender charges 2 points (2%) on a $100,000 loan, the origination fee would be $2,000.

Waiving the Fee

While it’s not common, there are scenarios where an origination fee might be waived or reduced:

- Fee-rate trade-off: Some lenders may be willing to eliminate the origination fee in exchange for a higher interest rate. For instance, if a lender quotes 8% interest plus 2 points, they might offer 11% interest with 0 points instead.

- Larger loan amounts: For substantial loan amounts, some lenders may be willing to reduce or waive the origination fee.

- Repeat business: Established borrowers with a strong track record might negotiate lower fees.

- Competitive market: In highly competitive markets, lenders might offer more favorable terms, including lower origination fees.

LTC

LTC (Loan-to-Cost) ratio is the percentage of the total project cost that a lender is willing to finance through a hard money loan. It compares the loan amount to the total cost of the property, including both the purchase price and any renovation costs.

Calculation

The LTC is calculated using this formula:

LTC = Loan Amount / Total Project Cost

For example, if a property costs $100,000 to purchase and requires $50,000 in renovations (total cost of $150,000), and the lender offers a loan of $120,000, the LTC would be:$120,000 / $150,000 = 0.80 or 80%

Key Concepts

Reserves

Reserve requirements are typically evaluated on a case-by-case basis, considering factors like the loan amount, project complexity, and borrower experience. Higher-risk projects or less experienced borrowers may require more substantial reserves.

Reserve requirements serve several important purposes in hard money lending:

- Risk mitigation: Reserves help mitigate the lender’s risk by ensuring the borrower has funds available to cover unexpected expenses or delays.

- Covering holding costs: Reserves can be used to pay for holding costs such as property taxes, insurance, and HOA fees during the loan term.

- Meeting loan payments: They ensure the borrower can make monthly loan payments, especially if the project experiences delays or setbacks.

- Handling unexpected expenses: Reserves provide a buffer for unanticipated renovation costs or other unforeseen expenses.

- Demonstrating financial stability: Adequate reserves show the lender that the borrower is financially stable and capable of managing the project.

- Preventing defaults: By having reserves, borrowers are less likely to default on their obligations to the lender, the state, or other creditors.

Cash to Close

This is the cash required which includes the downpayment, escrows, insurance, title fees, lender fees and other line items.

Liquidity Required

Liquidity Required = “Cash to Close” + “Reserves”